We’ve given big, privately owned banks the right to create money out of thin air.

They lend it to you for a while, if you can prove that there’s no risk involved.

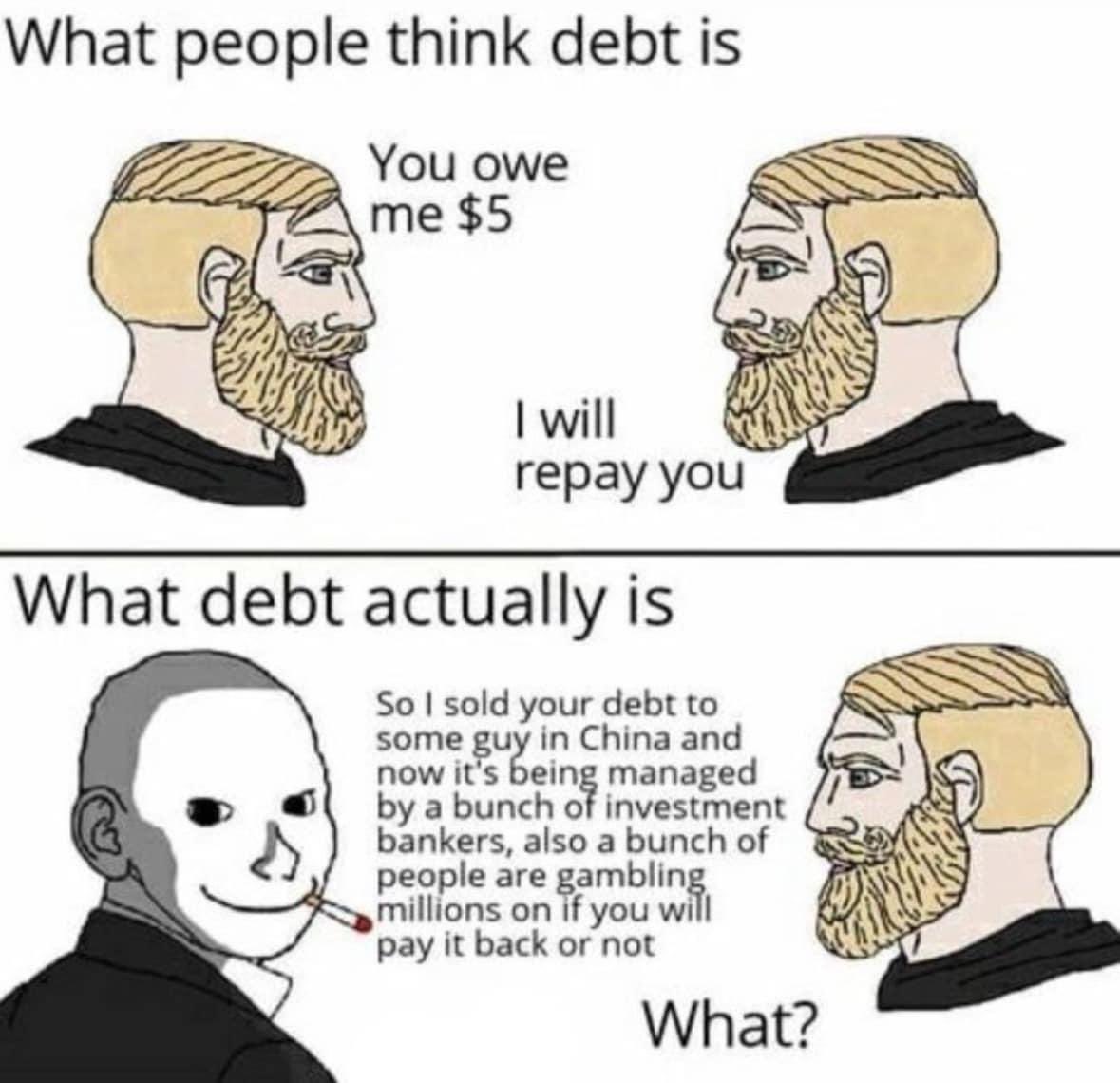

You still have to pay them back a lot more than you got.

Once you’ve given the money back, it disappears.

The banks keep the interest, though. And can use it to create 10x more money out of thin air.

Man, if it were just this then banks would be pretty stable.

The problem is banks don’t just lend and receive money, they invest. And they invest in everything. And they take super risky bets.

This is what caused the banking collapse of 2008 and what caused the death of SVB and a few other banks.

Your bank doesn’t just hold your money and debt, if you rent it almost certainly owns a peice of the company managing your property. It owns crypto assets. It has shares of startups. And it uses those assets to get more money to create more debt.

Dobb Frank was created to stop some of this, but unfortunately it’s been effectively repealed already.

Yup, and banks are returning to high-risk securities, trading in debt-based products like collateralized loan obligations, just like they did leading up to the 2008 global financial crisis.

And Dodd-Frank was passed as a weak facsimile of the previously-repealed Glass-Stegall act that was written after the Great Depression and effectively prevented any major financial collapses for 70 years.

We created this money to give to you, and you have to pay it back plus a 5-20% fee.

We’re also betting on whether you will pay it back or not, and other people are betting on whether our bet will win.

If we lose too many bets, or too many people bet against our bets, then the money we just gave you disappears, the economy crashes, and you get kicked out of your house.

Fractional reserve banking and the modern securities market is a trip. Kafka was on to something.

It’s not out of thin air, it’s out of your account, and everyone else’s too. They’re banking (heh) on most people not needing most of their money all at once. They keep a required reserve amount for people to actually withdraw. If all of the sudden everyone wants all of their money then that’s a run on the bank and it collapses.

No, it is actually out of thin air.

When a bank gives out a credit, that money is created on the spot, not drawn from somewhere.

There are rules as to how much money a bank is allowed to create, based on how much they actually have.

But no account of any kind is reduced by the amount they give out as credit.

You deposit 100 and I deposit 100, bank is required to keep 10 percent in cash (for example) that allows for 180 in loanable cash.

The bank loans out 180 dollars, now you have 100, I have 100 and someone else has 180, that money has been ‘created’ out of thin air.

The banks count on the fact that that me and you won’t both withdraw all of our money at once.

When banks finish the day, they actually check and see if they are within all of the margin limits that are required and do overnight loans from other banks to stay legal.

Money hasn’t been printed, but for the bookkeeping, 3 individuals who have contributed a total of 200 dollars, have in their accounts 380 dollars.

When a bank loans your money out, as we are well aware, they don’t change the account in your balance. In order to do that, the dollar being loaned must be duplicated somehow. This is normal to how fractional banking works, and guidelines and requirements for how much specific money you need to maintain doesn’t change that.

The only way to change it is to switch to full reserve banking.

If a bank is able to loan out your money, without also removing it from your account, it is by nature created, the money is in two places at once.

They don’t reduce your available balance because they’re constantly juggling the money around. But they’re not producing money out of thin air. They can’t loan more than they hold in deposits.

no but y y youre youre youre youre y you’re saying the money’s in Joe’s house, th thats that’s right next to yours, and and and and the Kennedy House, and Mrs Maitlin’s house and a hundred others.

w w why w why why why whaddaya want the Moon, Mary? L L L Lemme throw a LASSoo around it.

Unless you’re really rich, you have the choice between borrowing money from the bank, and paying rent to a landlord for your entire life.

Unless you’re moderately rich, you don’t even have that choice.

{kind=link}

What it actually is:

Man, if it were just this then banks would be pretty stable.

The problem is banks don’t just lend and receive money, they invest. And they invest in everything. And they take super risky bets.

This is what caused the banking collapse of 2008 and what caused the death of SVB and a few other banks.

Your bank doesn’t just hold your money and debt, if you rent it almost certainly owns a peice of the company managing your property. It owns crypto assets. It has shares of startups. And it uses those assets to get more money to create more debt.

Dobb Frank was created to stop some of this, but unfortunately it’s been effectively repealed already.

Yup, and banks are returning to high-risk securities, trading in debt-based products like collateralized loan obligations, just like they did leading up to the 2008 global financial crisis.

https://www.theguardian.com/business/2024/nov/24/remember-the-global-financial-crisis-well-high-risk-securities-are-back

Bank: You should take out this loan you can’t afford to repay. Don’t worry, we’ll make it seem like a great idea.

Unqualified borrower: Ok, since you made it seem like a great idea.

Bank: Great! Hey, other bank, betcha this guy won’t repay this loan.

And Dodd-Frank was passed as a weak facsimile of the previously-repealed Glass-Stegall act that was written after the Great Depression and effectively prevented any major financial collapses for 70 years.

1000%

Fractional reserve banking and the modern securities market is a trip. Kafka was on to something.

It’s not out of thin air, it’s out of your account, and everyone else’s too. They’re banking (heh) on most people not needing most of their money all at once. They keep a required reserve amount for people to actually withdraw. If all of the sudden everyone wants all of their money then that’s a run on the bank and it collapses.

No, it is actually out of thin air.

When a bank gives out a credit, that money is created on the spot, not drawn from somewhere.

There are rules as to how much money a bank is allowed to create, based on how much they actually have.

But no account of any kind is reduced by the amount they give out as credit.

Incorrect. Try starting your own bank and doing that. No other banks will do business with you and you’ll run out of money to give your borrowers.

This is how banks work.

You deposit 100 and I deposit 100, bank is required to keep 10 percent in cash (for example) that allows for 180 in loanable cash.

The bank loans out 180 dollars, now you have 100, I have 100 and someone else has 180, that money has been ‘created’ out of thin air.

The banks count on the fact that that me and you won’t both withdraw all of our money at once.

When banks finish the day, they actually check and see if they are within all of the margin limits that are required and do overnight loans from other banks to stay legal.

Look up fractional reserved banking.

Not correct. Your liabilities need to be sufficiently smaller than your assets. Capital reserves don’t need to be in cash.

200 dollars went in. 180 dollars came out. 20 dollars stay in the bank. No dollars have been created.

Look up solvency frameworks

Money hasn’t been printed, but for the bookkeeping, 3 individuals who have contributed a total of 200 dollars, have in their accounts 380 dollars.

When a bank loans your money out, as we are well aware, they don’t change the account in your balance. In order to do that, the dollar being loaned must be duplicated somehow. This is normal to how fractional banking works, and guidelines and requirements for how much specific money you need to maintain doesn’t change that.

The only way to change it is to switch to full reserve banking.

If a bank is able to loan out your money, without also removing it from your account, it is by nature created, the money is in two places at once.

Person A’s account: $100 Person B’s account: $100 Person C’s account: -$180

This does not add up to $380.

They don’t reduce your available balance because they’re constantly juggling the money around. But they’re not producing money out of thin air. They can’t loan more than they hold in deposits.

Uh… Yeah they can? Look up fractional reserve banking.

no but y y youre youre youre youre y you’re saying the money’s in Joe’s house, th thats that’s right next to yours, and and and and the Kennedy House, and Mrs Maitlin’s house and a hundred others.

w w why w why why why whaddaya want the Moon, Mary? L L L Lemme throw a LASSoo around it.

I sampled that scene in one of my songs.

Precisely. That scene made so much more sense to me after I took a financial accounting class in college.

Yep. Just don’t borrow it, fuck em.

Unless you’re really rich, you have the choice between borrowing money from the bank, and paying rent to a landlord for your entire life.

Unless you’re moderately rich, you don’t even have that choice.

If people could buy housing without needing to borrow money, the world would be a much better place.